Saving moneyis a fundamental aspect of personal finance, but determining how much you should save each month can be a daunting task. Many factors come into play, such as your financial goals, income level, and expenses.

It's a question that often lingers in the minds of individuals seeking to secure their financial future. Whether you're aiming to build an emergency fund, save for a down payment on a house, or plan for retirement, the question of "How much should I save each month?" is one that deserves careful consideration.

Let's get to know various approaches, guidelines, and strategies to help you determine the right amount to save each month and make progress toward your financial objectives.

How Much Money Should I Save Each Month?

Determining how much moneyyou should save each month can be challenging, but it depends on your goals and financial situation. Here are some factors to consider when deciding how much to save:

Set Clear Savings Goals

Identify what you're saving for, such as an emergency fund, a down payment on a house or car, or a vacation. Each goal will require a different amount of savings.

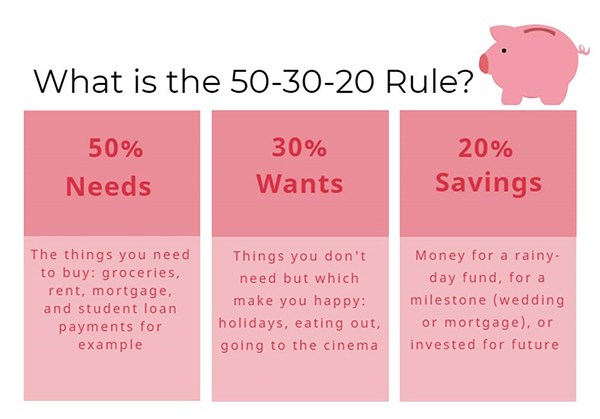

The 50/30/20 Rule

This budgeting rule suggests allocating 50% of your monthly income for essentials, 30% for wants, and 20% for savings. The 20% can be divided between various savings goals.

General Savings Guidelines

While there is no one-size-fits-all percentage, a common recommendation is to save between 10% and 20% of your income each month. Start with what you can afford and gradually increase your savings over time.

Evaluate Your Expenses

Track your spending to identify areas where you can cut back. Small adjustments, such as reducing discretionary expenses, can free up more money for savings.

Prioritize Emergency Savings

Aim to build an emergency fund that covers 3-9 months of living expenses. Start by calculating your monthly cost of living and gradually save towards this goal.

Consider Retirement Savings

Allocate a portion of your monthly savings to retirement accounts, such as a 401(k) or an IRA. A common recommendation is to save 10-15% of your income for retirement.

Make Saving A Habit

Start small if necessary and gradually increase your savings over time. Automate your savings by setting up automatic transfers from your paycheck or checking account to your savings account.

Remember, everyone's financial situation is unique, so adjust these guidelines to fit your needs. It's important to regularly assess and adjust your savings strategy as your circumstances change.

How To Use The 50-30-20 Rule To Plan Your Monthly Savings

The 50/30/20 rule is a budgeting guideline that can help you allocate your income effectively. Here's how you can use it to plan your monthly savings:

- Calculate your after-tax income - Start by determining how much money you bring home after taxes each month.

- Allocate 50% to essentials - Assign 50% of your income to cover essential expenses such as housing, groceries, utilities, transportation, and insurance.

- Allocate 30% to wants - Allocate 30% of your income to non-essential expenses or discretionary spending, such as dining out, entertainment, hobbies, and shopping.

- Allocate 20% to savings and debt repayment- Set aside 20% of your income for savings and debt repayment. This category includes contributions to emergency savings, retirement accounts, paying off high-interest debt, and saving for long-term goals like a down payment on a house.

- Customize your savings allocation- Within the 20% savings category, allocate funds based on your specific goals and financial situation. For example, you might allocate a portion to an emergency fund, retirement savings, and other financial goals.

Remember, the 50/30/20 rule is a guideline, and you can adjust the percentages to better suit your needs. If you have higher debt or savings goals, you may need to allocate more than 20% to savings and reduce spending in other categories.

Regularly review and adjust your budget as necessary to ensure you're making progress toward your financial goals.

How Much Of My Income Should I Save Each Month?

The amount of income you should save each month depends on your financial goals and individual circumstances. While there is no one-size-fits-all answer, here are some general guidelines to consider:

How Much of Your Paycheck Should You Save? (With Data)

The 20% Rule

Many financial experts suggest saving at least 20% of your income each month. This includes contributions to emergency savings, retirement accounts, and other long-term savings goals.

Pay Yourself First

Make saving a priority by setting aside a portion of your income before allocating funds to other expenses. Automate your savings by setting up automatic transfers from your paycheck or checking account to your savings account.

Build An Emergency Fund

Aim to save 3-9 months' worth of living expenses in an emergency fund. Start by calculating your monthly expenses and gradually save towards this goal.

Retirement Savings

Allocate a portion of your income to retirement accounts, such as a 401(k) or an IRA. A common recommendation is to save 10-15% of your income for retirement.

Adjust Based On Your Goals And Circumstances

Consider your short-term and long-term financial goals, as well as your income, expenses, and debt obligations. Adjust your savings rate accordingly to ensure you're making progress towards your goals while maintaining a sustainable budget.

Saving money is a personal financial decision, and it's important to find a balance that works for you. Start with what you can afford and gradually increase your savings over time as your income and financial situation improves.

How Much Money Can The Average Person Save Each Month?

The amount of money the average person can save each month varies depending on individual circumstances, such as income level, expenses, and financial goals. Here are some factors to consider when estimating how much the average person can save:

Income

Higher incomes generally allow for higher savings potential. However, even individuals with lower incomes can still save by adjusting their spending habits and making saving a priority.

Expenses

The average person's expenses, including housing, transportation, groceries, and debt payments, can significantly impact their ability to save. By carefully managing expenses and finding ways to reduce discretionary spending, individuals can free up more money for savings.

Financial Goals

The amount someone can save each month may vary depending on their specific financial goals. Individuals saving for short-term goals like a vacation or a down payment on a home may be able to save more in the short term, while those saving for long-term goals like retirement may contribute a smaller percentage each month.

Budgeting And Financial Habits

Developing good financial habits, such as budgeting, tracking expenses, and setting savings targets, can help the average person save more each month. Regularly reviewing and adjusting the budget can identify areas where savings can be increased.

7 Tips On How To Save Money Each Month

Saving money each month is an essential part of personal finance. Here are seven tips to help you save more:

7 Ways to Save Money Each Month (even with a tight budget) | FRUGAL LIVING

- Track your spending- Monitor your expenses by keeping a record of your purchases. Use budgeting apps or spreadsheets to categorize your expenses and identify areas where you can cut back.

- Automate your savings - Set up automatic transfers from your paycheck or checking account to your savings account. By automating your savings, you ensure a consistent contribution each month without relying on manual transfers.

- Consider an IRA - If eligible, contribute to an Individual Retirement Account (IRA) to boost your retirement savings. A Roth IRA, in particular, offers tax advantages and potential growth.

- Start small - Even if you can't save a large amount initially, start with a small, manageable sum. Consistency is key, and small savings can accumulate over time.

- Increase your savings over time - Gradually increase the amount you save each month as your income allows. Set specific goals to increase your savings rate annually or semi-annually.

- Review your subscriptions and services- Regularly assess your subscriptions, memberships, and services to identify any that you no longer use or need. Cancelling unused or unnecessary subscriptions can free up extra money for savings.

- Take advantage of windfalls- When you receive unexpected income, such as a tax refund or a work bonus, allocate a portion of it to savings. This allows you to boost your savings without affecting your regular monthly budget.

Saving money requires discipline and conscious decision-making. By implementing these tips and making saving a priority, you can develop healthy financial habits and achieve your savings goals.

People Also Ask

How Much Money Should I Have Saved By 30?

It is recommended to have at least six months' worth of income saved by age 30. Life is unpredictable, and having a savings cushion is crucial for emergencies such as job loss or illness.

How Much You Should Save By Month And By Age?

Savings benchmarks:

- Age 30 - Aim to have an amount equal to your annual salary saved.

- Age 40- Target saving three times your income.

- Age 50- Strive for savings six times your income.

- Age 60- Aim to have saved eight times your income.

Can I Retire With 2 Million At 50?

Retiring at the age of 50 with $2 million is feasible. With an annuity, you can receive a guaranteed income of $125,000 per year starting immediately and continuing for the rest of your life. The income remains constant and is adjusted periodically to account for inflation.

How Much Should A 22 Year Old Save?

A commonly followed guideline suggests saving 20% of your salary for retirement, emergencies, and long-term goals.

Is 22 Too Late To Start Saving?

Regardless of your age, it is always possible to start saving for retirement. However, as you get older, certain factors such as retirement goals and required minimum distributions (RMDs) may impose limitations on your options.

What Age Is Best To Save Money?

In your 20s, it is recommended to have an emergency fund that covers three to six months of your expenses, according to Bankrate. CNN Money advises starting to save for long-term retirement goals as soon as you finish school.

Should I Save Money In My 20s?

Building savings early on can provide you with a significant advantage. Even if you have to make adjustments for careeradvancement or starting a family, saving in your 20s can pave the way for greater opportunities in your 30s and beyond. By setting aside funds during your 20s, you can create the potential to enjoy more financial freedom and flexibility later in life.

Conclusion

In conclusion, the question of "How much should I save each month?" is one that has no one-size-fits-all answer. It depends on your unique circumstances, goals, and financial situation.

The key is to find a balance that allows you to save consistently while still meeting your daily needs and enjoying life. Remember, saving money is a habit that requires discipline and commitment. Start by assessing your financial goals, tracking your expenses, and implementing strategies to increase your savings over time.

Whether you start with a small amount or aim for a specific percentage of your income, the most important thing is to take action and begin saving. As you progress in your financial journey, regularly review and adjust your savings plan to ensure you're making meaningful progress towards your goals.

With determination and smart financial habits, you can achieve your savings objectives and build a solid foundation for a secure and prosperous future. So, ask yourself, "How much should I save each month?" and take the first step on your savings journey today.