Annual portfolio rebalancingis the financial maneuver that serves as the compass directing your investments toward continued growth and stability. Picture this: just as a gardener tends to their garden, carefully pruning and nurturing different plants to ensure a harmonious and flourishing landscape, annual portfolio rebalancing involves a meticulous review and adjustment of your investment allocations.

This financial practice is not merely about tinkering with numbers; it's about preserving and enhancing your financial well-being. Through annual portfolio rebalancing, investors mitigate risks by ensuring their portfolio aligns with their long-term objectives while optimizing returns. It's a proactive approach that not only safeguards your investments against market fluctuations but also ensures your financial goals.

Rebalance Your Portfolio To Stay On Track

Rebalancing your portfolio is like tuning up your car, it's essential for keeping it running smoothly and efficiently towards your financial goals. Just as a car's performance can decline over time due to wear and tear, your portfolio's asset allocation can drift away from your target mix because of market movements and individual asset performance. This drift can expose you to unintended risk and hinder your progress towards your goals.

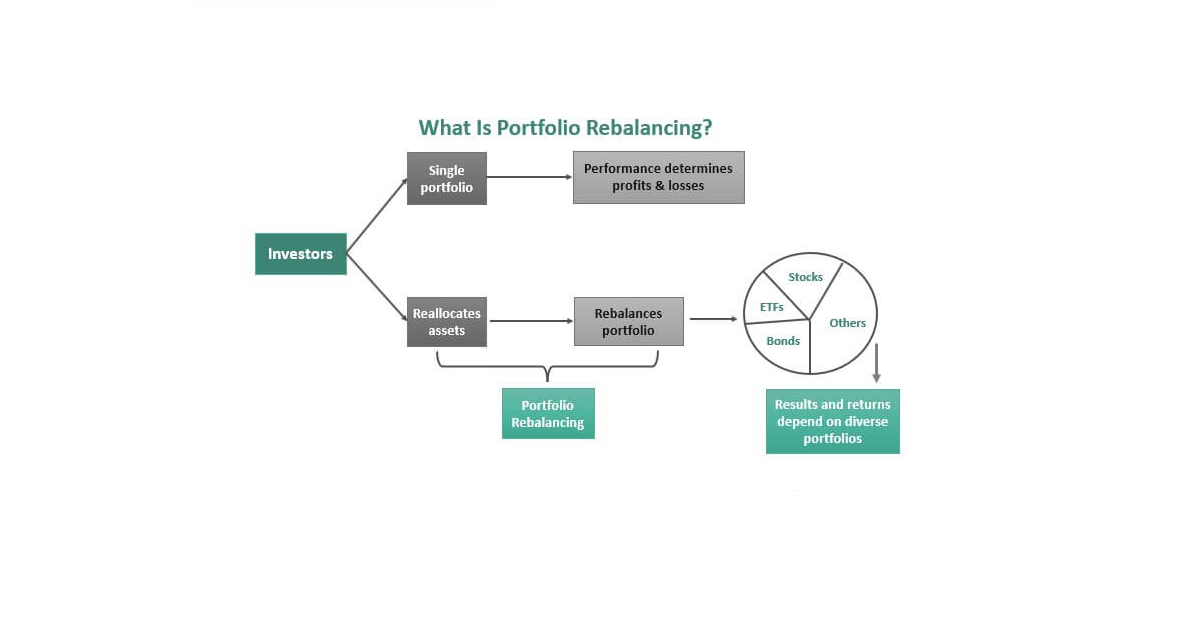

What Is Portfolio Rebalancing?

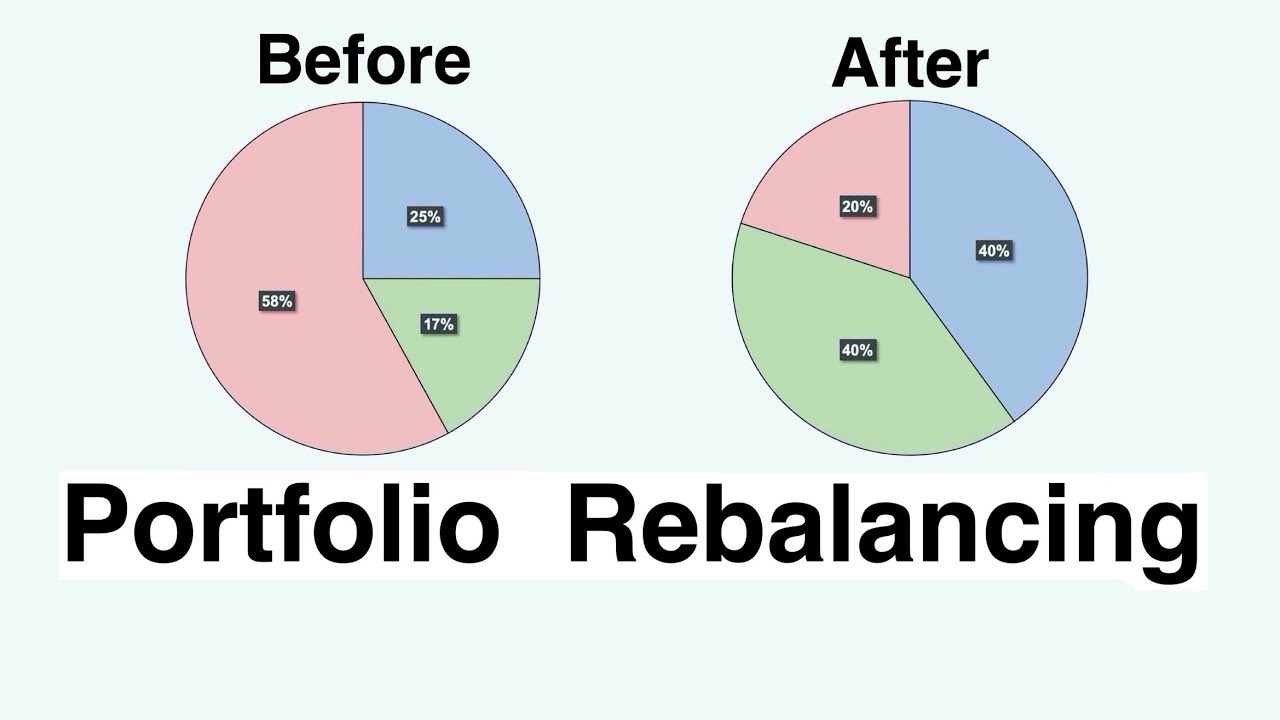

Portfolio rebalancing is the process of adjusting the weights of different asset classes in your portfolio to bring them back in line with your target allocation. Think of it like redistributing the moneyyou've invested across different asset classes to maintain your desired level of risk and return.

Why Is Rebalancing Important?

1. Maintains your desired risk exposure -Over time, market movements can cause certain asset classes in your portfolio to outperform others, leading to an imbalance in your overall risk profile. Rebalancing helps to correct this imbalance and keep your risk exposure within your comfort zone.

2. Boosts long-term returns -Studies have shown that rebalancing can actually enhance your portfolio's return over the long term. This is because it forces you to sell assets that have become overvalued and buy those that have become undervalued, taking advantage of market cycles.

3. Improves discipline -Rebalancing takes the emotion out of investing by forcing you to stick to your long-term plan, regardless of what's happening in the short term.

When To Rebalance Your Portfolio?

There's no one-size-fits-all answer to this question, as the frequency of rebalancing will depend on your individual circumstances and risk tolerance. However, some general guidelines include:

- Annually -This is a common and convenient timeframe for most investors.

- When asset allocations deviate significantly -If your asset allocations have drifted by more than 5-10% from your target, it may be time to rebalance.

- After major life changes -Significant life eventssuch as retirement or a job change may necessitate a review and potential rebalancing of your portfolio.

How To Rebalance Your Portfolio?

- Review your target asset allocation -This is the blueprint for your portfolio and should reflect your risk tolerance and financial goals.

- Calculate your current asset allocation -Determine the percentage of your portfolio invested in each asset class.

- Compare your target and current allocations -Identify any imbalances that need to be corrected.

- Develop a rebalancing strategy -Decide which assets to buy or sell to bring your portfolio back in line with your target allocation. You can choose to rebalance proportionally (adjusting all asset classes) or strategically (focusing on undervalued assets).

- Execute your trades -Make the necessary trades to implement your rebalancing strategy.

- Monitor and repeat -Rebalancing is an ongoing process, so be sure to monitor your portfolio regularly and repeat the process as needed.

7 Steps For Annual Portfolio Rebalancing - A Comprehensive Guide

Annual portfolio rebalancing is a crucial exercisefor investors to maintain their desired asset allocation and stay on track with their financial goals. It involves reviewing your portfolio holdings, making adjustments to bring them back in line with your target allocations, and selling underperforming assets while potentially buying new ones.

Here are 7 crucial steps for successful annual portfolio rebalancing:

1. Review Your Target Asset Allocation

Before making any adjustments, revisit your target asset allocation. This refers to the percentage of your portfolio you want to allocate to different asset classes like stocks, bonds, cash, and alternative investments. Consider your risk tolerance, time horizon, and financial goals when determining your target allocation.

2. Calculate Portfolio Drift

Compare your current asset allocation with your target allocation. This will reveal any drift that has occurred due to market movements or individual asset performance. Calculate the percentage difference for each asset class to understand the extent of the drift.

3. Determine Rebalancing Needs

Decide if rebalancing is necessary based on the magnitude of the drift. Some experts recommend rebalancing when asset allocations deviate by more than 5% from the target, while others suggest a 10% threshold. Consider your individual circumstances and risk tolerance when making this decision.

4. Choose Rebalancing Strategies

There are two main rebalancing strategies: proportionaland strategic. Proportional rebalancing involves adjusting all asset classes back to their target weights, while strategic rebalancing focuses on buying undervalued assets and selling overvalued ones. Choose the strategy that aligns with your investment philosophy and risk tolerance.

5. Execute Rebalancing Transactions

Once you've decided on your rebalancing strategy, it's time to execute the trades. Consider tax implications when selling assets, and try to minimize transaction costs to maximize efficiency. You can rebalance manually or use automated tools provided by some brokerages.

6. Reassess And Adjust

Rebalancing is an ongoing process, not a one-time event. Regularly review your portfolio and repeat the rebalancing process annually or more frequently if needed. Market conditions and your personal circumstances may necessitate adjustments to your target asset allocation over time.

7. Seek Professional Guidance

If you're unsure about any aspect of rebalancing, consider seeking professional guidance from a financial advisor. They can help you determine your target asset allocation, develop a rebalancing strategy, and execute trades in a tax-efficient manner.

Additional Tips

- Automate rebalancing -Some brokerages offer automated rebalancing tools that can simplify the process. Consider using these tools if you want to make rebalancing a seamless part of your investment strategy.

- Harvest tax losses -If you need to sell assets to rebalance, consider selling underperforming assets to generate tax-deductible losses. This can offset capital gains and reduce your overall tax liability.

By following these steps and considering the additional tips, you can ensure that your annual portfolio rebalancing is a successful and beneficial exercise that helps you achieve your financial objectives.

How To Avoid Taxes When Rebalancing Investments

Uncle Sam has a way of taking a bite out of your investment returns, and rebalancing your portfolio is no exception. But fear not, there are ways to minimize the tax hit while keeping your asset allocation on track. Here are some strategies you can use:

1. Utilize Tax-advantaged Accounts

Retirement accounts -Invest in a traditional IRA or 401(k) where your contributions grow tax-deferred, meaning you won't pay taxes on them until you withdraw them in retirement. This is a great way to rebalance without worrying about capital gains taxes.

Roth accounts -Contributions to Roth IRAs and Roth 401(k)s are made with after-tax dollars, but withdrawals in retirement are tax-free. This gives you more flexibility to rebalance without tax consequences.

2. Implement Tax-loss Harvesting

Sell investments that have gone down in value to offset capital gains from other investments. This can lower your taxable income and potentially even create a tax refund. Just be sure to follow the wash-sale rule to avoid negating the benefits.

3. Rebalance Strategically

Instead of selling assets across the board, focus on selling those that have already generated capital losses or have low tax bases (the original purchase price of the asset). This way, you minimize the amount of taxable gains you realize.

4. Be Mindful Of Timing

Consider the tax implications of selling investments near the end of the year. You may be able to delay some sales until the following year to spread out your tax liability.

5. Seek Professional Guidance

- Consulting a financial advisor can help you develop a tax-efficient rebalancing strategy that aligns with your overall financial goals.

- Remember, every investor's situation is unique, so what works for one person may not be the best approach for another. It's crucial to consider your individual circumstances and risk tolerance when making any investment decisions.

- By incorporating these strategies and seeking professional advice if needed, you can navigate the tax complexities of rebalancing and keep more of your hard-earned moneyworking for you.

Additional Tips

- Keep detailed records of your investment transactions, including purchase dates and costs. This will make it easier to calculate your capital gains and losses for tax purposes.

- Be aware of the holding period requirements for capital gains taxes. Assets held for less than one year are taxed at your ordinary income tax rate, while those held for longer than one year are taxed at the lower capital gains rate.

- Consider the impact of state and local taxes on your rebalancing decisions.

Types Of Portfolio Rebalancing

When it comes to portfolio rebalancing, there's no one-size-fits-all approach. Different strategies cater to diverse investor needs and risk tolerances. Here's a breakdown of some common types of portfolio rebalancing:

1. Time-based Rebalancing

This is the most straightforward method, involving regular reviews and adjustments to your portfolio at predetermined intervals, often annually or quarterly. It's simple to implement but may not be responsive to immediate market fluctuations.

2. Constant-Mix Rebalancing

This approach focuses on maintaining a specific weight for each asset class in your portfolio. Whenever allocations stray beyond a predefined tolerance level, you rebalance to bring them back in line. This ensures consistent risk exposure but can be costly due to frequent trading.

3. Constant Proportion Portfolio Insurance (CPPI)

This dynamic strategy combines elements of aggressive and conservative investing. It sets a "floor" for your portfolio value by allocating a portion to conservative assets like bonds. If the portfolio dips below the floor, assets are sold to buy more bonds and protect your capital. Conversely, if it rises above the floor, bonds are sold to buy riskier assets for potential growth.

4. Percentage-of-Portfolio Rebalancing

This method uses a set percentage change as the trigger for rebalancing. For example, if your asset allocation deviates by more than 5% from your target, you adjust your holdings until they fall within the 5% threshold. This offers a balance between responsiveness and cost-effectiveness.

5. Strategic Rebalancing

This approach goes beyond simply buying or selling to reach your target allocation. It focuses on identifying undervalued and overvalued assets within your portfolio. You then strategically sell the overvalued ones and reinvest the proceeds in the undervalued ones. This requires more in-depth analysis but can potentially enhance long-term returns.

6. Smart Beta Rebalancing

This strategy involves investing in low-cost index funds or ETFs that track specific investment factors or strategies rather than traditional market capitalization indices. While it doesn't involve individual stock picking, it allows you to tilt your portfolio towards desired characteristics such as value or momentum while maintaining diversification.

The choice of rebalancing method depends on various factors, including:

- Risk tolerance -More cautious investors may favor time-based or constant-mix approaches, while those with higher risk tolerance can consider strategic or CPPI strategies.

- Investment goals -If your primary goal is income generation, focusing on fixed-income assets might be more suitable. If seeking long-term growth, a more equity-heavy allocation with strategic rebalancing may be appropriate.

- Transaction costs -Be mindful of trading costs, as frequent rebalancing can eat into your returns. Choose a method that balances responsiveness with cost efficiency.

How Often Should You Rebalance?

There's no one-size-fits-all answer to how often you should rebalance your portfolio, as the ideal frequency depends on several factors including:

1. Your Risk Tolerance

- Conservative investors -Might prefer less frequent rebalancing (annually or even biannually) to minimize transaction costs and maintain a stable asset allocation.

- Moderate investors -May opt for quarterly or biannual rebalancing, balancing responsiveness to market changes with cost efficiency.

- Aggressive investors -Might choose monthly or even more frequent rebalancing to capitalize on market fluctuations and potentially enhance returns, but this can lead to higher transaction costs.

2. Your Investment Goals

- Long-term goals -Investors with long-term investment horizons can afford less frequent rebalancing as market fluctuations over shorter periods tend to average out.

- Short-term goals -Those with short-term goals may benefit from closer monitoring and more frequent rebalancing to ensure their portfolio aligns with their immediate needs.

3. The Magnitude Of Portfolio Drift

- Small drift (less than 5%) -You might choose to hold off on rebalancing until the deviation becomes more significant.

- Large drift (more than 10%) -This indicates a need for rebalancing to maintain your desired risk exposure and potentially capitalize on undervalued assets.

4. Transaction Costs

Frequent rebalancing incurs more transaction costs, which can eat into your returns. Weigh the potential benefits of responsiveness against the cost implications.

General Guidelines

- Annual Rebalancing -This is a popular and convenient option for many investors, offering a balance between cost-effectiveness and responsiveness to market changes.

- Time-Based Rebalancing -You can set a pre-determined schedule (monthly, quarterly, etc.) for reviewing and rebalancing your portfolio.

- Threshold-Based Rebalancing -Rebalance only when asset allocations deviate from your target by a defined percentage.

Other Points To Consider

- Market Volatility -More volatile markets may necessitate more frequent rebalancing to manage risk exposure.

- Individual Asset Performance -Some assets may experience significant swings, prompting adjustments to maintain your desired allocation.

- Tax Implications -Consider tax consequences when selling assets for rebalancing, potentially utilizing tax-loss harvesting strategies.

FAQ's About Annual Portfolio Rebalancing

What Is An Example Of Rebalancing?

It involves the fees related to the transactions to purchase and sell securities. It can also involve the cost of performance. For example, to rebalance, you might sell securities that have increased in value and pushed your allocations out of whack.

Is Rebalancing Portfolio A Good Idea?

Rebalancing is important for two reasons: risk management and improved returns. An asset allocation plan is designed to accomplish two competing goals: optimal returns and minimal risk. Without rebalancing, many portfolios drift away from bonds and into more stock investments over time.

What Is The Principle Of Portfolio Rebalancing?

Portfolio Rebalancing is the process of buying and selling portions of your portfolio in order to set the weight of each asset class back to its pre-determined allocation. You may need to rebalance your portfolio periodically because the market value of each asset class changes over time due to different returns.

Conclusion

Annual portfolio rebalancing stands as a cornerstone of prudent financial management. It encapsulates the essence of adaptability and resilience in navigating the unpredictable waters of the financial markets. By embracing this disciplined approach, investors fortify their portfolios against undue risks and position themselves strategically to capitalize on market opportunities while safeguarding their long-term goals.

Ultimately, the true power of annual portfolio rebalancing lies not just in the numbers but in the sense of empowerment it bestows upon investors. It offers the assurance that they are actively steering their financial future, staying aligned with their objectives, and fostering resilience in the face of uncertainty.